Ashish Vohra

ED and CEO

Reliance Nippon Life Insurance

With the secular drop in interest rates in the last 3-4 years, your bank FD oriented financial planning may be at a big risk. For long-term investments, short-term volatility is of no concern. The real risk is falling woefully short of the required corpus for goals like child’s education, marriage or even retirement. In these uncertain times, life insurance products that guarantee return are the best solution. The life protection element in such products ensures that even if you die, your dear ones will always get the promised money.

You have been working hard and saving money in bank deposits by cutting expenses wherever possible. Your current family responsibilities notwithstanding, your child's education, marriage and your own retirement need lots of money, and is growing costlier as every year passes.

However, the rate reduction in interest given on bank deposits greatly impacts your financial planning. It is important that there is clarity on the amount of return expected after a fixed period of time, but with bank FDs at the moment there is none.

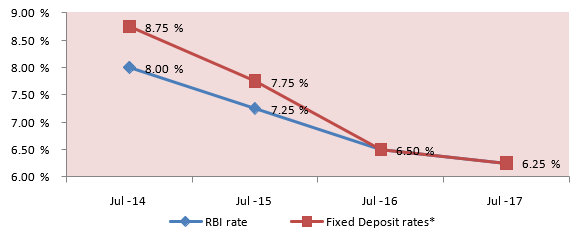

The chart below shows the trajectory of returns on Fixed Deposits falling in the period of interest rate cut at a similar pace.

*Fixed deposit rates considered for 5-10 years tenure for State Bank of India as disclosed in their website

Unprotected savings

With the repo rate at a seven-year low of 6%, bank deposits may fail to provide you with adequate returns. Economists and analysts are expecting more reduction, opening up the possibility of further reduced returns.

The difference between the annual interest earned on Rs 10 lakh as the rate of interest slipped from 8.75% to 6% in the last 3 years is about Rs 30,000 in just one year. Over 20-25 years, the drop in interest will greatly alter your financial savings plan as the rate of bank FD interest is also not fixed for such a long duration.

For example, you are planning to get to a magic figure of Rs 70 lakh in 20 years, you will need to save Rs 15,000 per month at 6% interest rate. However, if the interest rate is 4%, you will save only Rs 55 lakh. The gap of Rs 15 lakh could affect the plans of your child’s higher education like MBA, unless you increase your monthly savings rate to over Rs 19000 per month, which could be a severe challenge for your current responsibilities.

The declining interest rate scenario poses a huge risk to the segment of customers with low risk taking appetite, ability to understand the stock market, especially in the non-metro locations. They usually opt for investments with fixed returns like FDs.

Guaranteed returns

The time is therefore right for customers to understand and evaluate alternate investment options which offer guaranteed returns, irrespective of the changes in market conditions and interest rates.

One of the most attractive propositions in this scenario clearly is ‘life insurance’ especially the ones that offer ‘guaranteed returns’ with a life protection component. In comparison to FDs, good guaranteed return life insurance products offer better returns on a tax-adjusted basis.

These life insurance policies give a fixed return, and also come with the guarantee of payout if the life covered meets with untimely death. In this way, there is nothing left to chance when it comes to providing financial protection for your family.

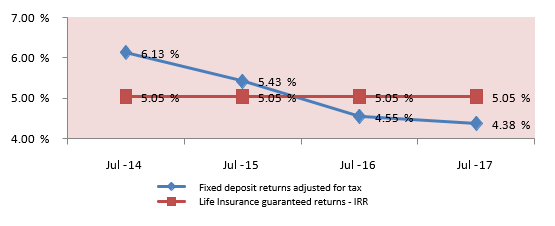

Here is a comparison of FD returns adjusted for taxes with a Guaranteed Return Life Insurance product

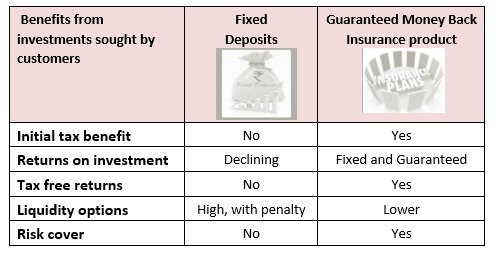

A guaranteed money back insurance product gives you initial tax benefit, fixed and tax-free returns, and a life protection cover. In comparison, most bank FDs do not offer any tax benefit, and there is no risk protection cover as well if you face premature death.

When the life assured dies during the term of the policy i.e. before date of maturity, proceeds under the policy are payable as a claim to the nominee. According to the data collated from Life Insurance Council, death claims paid by life insurance companies crossed Rs 19,000-crore mark in 2016-17.

The life insurance sector in India has also been constantly working towards creating higher value to customers through not just returns, but through improving servicing standards.

The chart below shows a comparative assessment of the two investment options which typically trigger a customer’s decision:

With insurance product returns becoming more lucrative than some of the other investment alternatives in the current scenario, savers should re-consider their financial plan and incorporate products that offer attractive guaranteed returns towards their long term goals that will need to be fulfilled. Consumers should understand the exact guaranteed cash flows of insurance policy for their age, difference from 'likely' cash flows as illustrated by insurers, conditions on premature closure, taxation benefits before making a purchase.

Caveat: Insurance is a matter of solicitation. Returns mentioned in this article are indicative. Please validate taxation benefits and exact guaranteed returns for the product you are considering.